Delaware

Taxation

Delaware is the country's corporate tax haven, with over half of its publicly held corporations registered there, including 58% of the Fortune 500. Corporations are attracted by Delaware's exemption from taxation of the subsidiaries of holding companies (so the holding-company headquarters are located in Delaware and the operating subsidiaries generally elsewhere). Financial institutions are attracted by its absence of usury limits. The fees paid by hundreds of thousands companies allow it to be one of five states with no sales tax. Combined state and local taxes in 2003 amounted to 7.3% of income, the 3rd smallest percentage in the US, ahead of only New Hampshire and Alaska. In Delaware's state tax revenues come primarily from levies on personal and corporate income, inheritance and estates, motor fuels, cigarettes, state lottery, and alcoholic beverages.

Delaware's individual income tax is a seven-bracket progressive schedule ranging from 2.2% to 5.55% for income under $60,000 and 5.95% for income over that amount. Personal exemptions are in the form of $110 tax credits per adult and per child. There is no general sales tax, but selective sales taxes (excises) are imposed on gasoline (23 cents per gallon) and other motor fuels, cigarettes (24 cents a pack) and other tobacco products, alcoholic beverages, amusements, insurance premiums, pari-mutuels, public utilities, and other selected items. The corporate income tax is a flat tax of 8.7%. As part of their business and occupational license fees, businesses are assessed a gross receipts tax ranging from 0.096% to 1.92%, with the highest rate applied to rentals. Except for rentals, license fees also include an annual flat fee (generally $75 per business establishment) and monthly exclusions from the gross receipts tax ($1million for manufacturers and $50,000 for most services). The annual franchise tax ranges from a minimum of $35 to a maximum of $165,000, calculated either according to the number of authorized shares in the company (the minimum applying to companies with 3,000 or fewer shares) or according to the assumed par value of capital (the minimum applying to assumed par values of less than $140,000, and the maximum reached at a par value of $660 million). As is true for most states, Delaware's estate tax is set equal to the federal exemption from the payment of the federal death tax for the payment of state death taxes (estate taxes), and is, therefore, scheduled to be phased out by 2007 in tandem with the phase-out of the federal tax credit, absent countervailing action by the state. Revenue losses from the phase-out of Delaware's estate tax are estimated at $7.6 million in 2003, $16.3 million in 2004, and $34.7 million in 2007. Delaware has repealed its gift tax. Other taxes include various state license fees, a lodging tax, a realty transfer tax and local property taxes.

In 2003, state tax collections totaled $2.174 billion, or $2,692 per capita, including 36% from licenses, 33% from individual income taxes, 14.8% from selective sales taxes, 11.5% from corporate income taxes, and 1.9% from death and gift taxes.

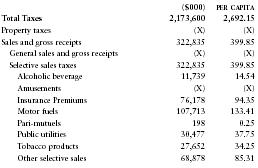

The following table from the US Census Bureau provides a summary of taxes collected by the state in 2002.

| ($000) | PER CAPITA | |

| Total Taxes | 2,173,600 | 2,692.15 |

| Property taxes | (X) | (X) |

| Sales and gross receipts | 322,835 | 399.85 |

| General sales and gross receipts | (X) | (X) |

| Selective sales taxes | 322,835 | 399.85 |

| Alcoholic beverage | 11,739 | 14.54 |

| Amusements | (X) | (X) |

| Insurance Premiums | 76,178 | 94.35 |

| Motor fuels | 107,713 | 133.41 |

| Pari-mutuels | 198 | 0.25 |

| Public utilities | 30,477 | 37.75 |

| Tobacco products | 27,652 | 34.25 |

| Other selective sales | 68,878 | 85.31 |

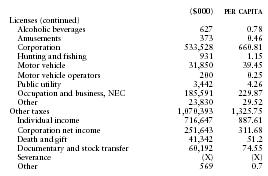

| ($000) | PER CAPITA | |

| Licenses (continued) | ||

| Alcoholic beverages | 627 | 0.78 |

| Amusements | 373 | 0.46 |

| Corporation | 533,528 | 660.81 |

| Hunting and fishing | 931 | 1.15 |

| Motor vehicle | 31,850 | 39.45 |

| Motor vehicle operators | 200 | 0.25 |

| Public utility | 3,442 | 4.26 |

| Occupation and business, NEC | 185,591 | 229.87 |

| Other | 23,830 | 29.52 |

| Other taxes | 1,070,393 | 1,325.75 |

| Individual income | 716,647 | 887.61 |

| Corporation net income | 251,643 | 311.68 |

| Death and gift | 41,342 | 51.2 |

| Documentary and stock transfer | 60,192 | 74.55 |

| Severance | (X) | (X) |

| Other | 569 | 0.7 |