Indiana

Taxation

The first state property tax in Indiana was levied in 1852 to support public schools.

In 1923, a state gasoline tax of 2 cents per gallon was introduced. (It ranged from 11.1 cents to 14 cents in 1984, depending on average prices in a specified month) In 2003 the gasoline tax was 15 cents a gallon. In 2002, Indiana was one of 20 states to increase its tax on a pack of cigarettes, and its increase, from 15.5 cents to 55.5 cents, was the biggest percent increase in the group. Indiana imposes a full set of excise taxes—on tobacco products, alcoholic beverages, motor fuels, parimutuels, public utilities, amusements, and other selected items.

In 1933, Indiana instituted the personal income tax, which was the major source of state revenue until 1963, when a 2% retail sales tax was enacted. In 1973, the state sales tax was doubled to 4% and optional local income taxes of up to 1% were initiated, while local property taxes were reduced by at least 20% to ease the tax burden on property owners. In 1983, the state sales tax was raised to 5%, and in 2002, Indiana raised the rate to 6%, one of two states to increase its general sales rate that year. Local option sales taxes, however, have been abolished. The state's personal income tax is a flat 3.4% of adjusted gross income with personal and child exemptions of $1000 each. The corporate tax rate was increased from 3.4% to 8.5% in 2003, which was the rate being applied only to financial institutions. The state estate tax, with a maximum rate of 15%, is established in Indiana law independently of the federal exemption for state death taxes, and therefore is unaffected by the phasing out of the federal estate tax credit by 2007. Indiana's inheritance tax ranges from 1% to 10% of fair market value of property transferred ate death. State death and gift taxes accounted for 1.4% of state collections in 2002. Other taxes include various state license fees and 1% petroleum production tax.

In fiscal 2002, state tax collections totaled $6.159 billion, 38% generated by the state sales and use tax, 35.4% by the state personal income tax, 15.4% by state excise taxes, 6.6% by the state corporate income tax, and 3% from license fees. Combined state and local taxes, of which the state portion is about 56.6% (2000 est.), amount to 9.7% of income, with Indiana ranking 22nd in terms of state and local tax burden in 2003.

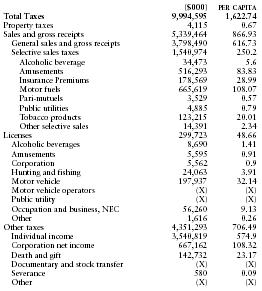

The following table from the US Census Bureau provides a summary of taxes collected by the state in 2002.

| ($000) | PER CAPITA | |

| Total Taxes | 9,994,595 | 1,622.74 |

| Property taxes | 4,115 | 0.67 |

| Sales and gross receipts | 5,339,464 | 866.93 |

| General sales and gross receipts | 3,798,490 | 616.73 |

| Selective sales taxes | 1,540,974 | 250.2 |

| Alcoholic beverage | 34,473 | 5.6 |

| Amusements | 516,293 | 83.83 |

| Insurance Premiums | 178,569 | 28.99 |

| Motor fuels | 665,619 | 108.07 |

| Pari-mutuels | 3,529 | 0.57 |

| Public utilities | 4,885 | 0.79 |

| Tobacco products | 123,215 | 20.01 |

| Other selective sales | 14,391 | 2.34 |

| Licenses | 299,723 | 48.66 |

| Alcoholic beverages | 8,690 | 1.41 |

| Amusements | 5,595 | 0.91 |

| Corporation | 5,562 | 0.9 |

| Hunting and fishing | 24,063 | 3.91 |

| Motor vehicle | 197,937 | 32.14 |

| Motor vehicle operators | (X) | (X) |

| Public utility | (X) | (X) |

| Occupation and business, NEC | 56,260 | 9.13 |

| Other | 1,616 | 0.26 |

| Other taxes | 4,351,293 | 706.49 |

| Individual income | 3,540,819 | 574.9 |

| Corporation net income | 667,162 | 108.32 |

| Death and gift | 142,732 | 23.17 |

| Documentary and stock transfer | (X) | (X) |

| Severance | 580 | 0.09 |

| Other | (X) | (X) |