Minnesota

Taxation

Corporate profits are taxed at a flat rate of 9.8%.There is an alternative minimum tax (AMT) with a 5.8% rate. Effective 2001/02, personal income tax rates on Minnesota's three-bracket schedule were lowered, the lowest rate from 5.5% to 5.3% (on taxable income up to $18,710 for singles, and up to $27,350 for couples), and the highest from 8% to 7.85% (on taxable income above $61,461 for single, and $108,661 for couples). Personal exemptions and the standard deduction are the same as for federal income tax, and tax brackets are indexed for inflation. A refundable earned income credit is provided for low-income workers. The state of Minnesota also levies a 6.5% state sales tax, with local-option sales taxes permitted up to 1%. Food, medicines and other basics are exempted. The state also imposes a full array of excise taxes covering motor fuels, tobacco products, insurance premiums, public utilities, alcoholic beverages, amusements, pari-mutuels, and many other selected items. In 1980, Minnesota tied its estate tax to the federal exemption for state death taxes, but has reinstated its independent tax since the federal estate tax credit has been scheduled to be phased out by 2007. Death and gift taxes accounted for 0.6% of state taxes collected in 2002. Other state taxes include per ton severance taxes (for taconite, iron sulphides, agglomerate, and semi-taconite), various license fees, and stamp taxes.

Real property (commercial, industrial, and residential) is subject to the property tax, which accounts for 95% of total tax collections by local governing units. In Minnesota's classified property tax system, commercial, industrial, and rental properties are taxed at considerably higher rates than owned homes. Minnesota's "circuit breaker" system refunds property tax payments to homeowners and renters whose residential property taxes are high relative to their income. In 2002, about 37% of total state and local taxes were collected at the local level.

Total state tax collections in Minnesota in 2002 were $12.936 billion, of which 42.1% was generated by the state income tax, 28.9% by the state general sales and use tax, 15.7% by state excise taxes, 6.7% by state license fees, and 4.3% by the state corporate income tax. In 2003, Minnesota ranked 11th among the states in terms of state and local tax burden, which amounted to about 11% of income.

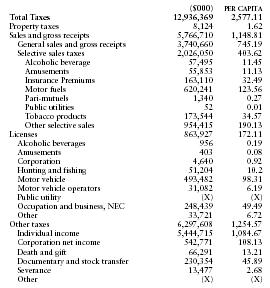

The following table from the US Census Bureau provides a summary of taxes collected by the state in 2002.

| ($000) | PER CAPITA | |

| Total Taxes | 12,936,369 | 2,577.11 |

| Property taxes | 8,124 | 1.62 |

| Sales and gross receipts | 5,766,710 | 1,148.81 |

| General sales and gross receipts | 3,740,660 | 745.19 |

| Selective sales taxes | 2,026,050 | 403.62 |

| Alcoholic beverage | 57,495 | 11.45 |

| Amusements | 55,853 | 11.13 |

| Insurance Premiums | 163,110 | 32.49 |

| Motor fuels | 620,241 | 123.56 |

| Pari-mutuels | 1,340 | 0.27 |

| Public utilities | 52 | 0.01 |

| Tobacco products | 173,544 | 34.57 |

| Other selective sales | 954,415 | 190.13 |

| Licenses | 863,927 | 172.11 |

| Alcoholic beverages | 956 | 0.19 |

| Amusements | 403 | 0.08 |

| Corporation | 4,640 | 0.92 |

| Hunting and fishing | 51,204 | 10.2 |

| Motor vehicle | 493,482 | 98.31 |

| Motor vehicle operators | 31,082 | 6.19 |

| Public utility | (X) | (X) |

| Occupation and business, NEC | 248,439 | 49.49 |

| Other | 33,721 | 6.72 |

| Other taxes | 6,297,608 | 1,254.57 |

| Individual income | 5,444,715 | 1,084.67 |

| Corporation net income | 542,771 | 108.13 |

| Death and gift | 66,291 | 13.21 |

| Documentary and stock transfer | 230,354 | 45.89 |

| Severance | 13,477 | 2.68 |

| Other | (X) | (X) |