Nebraska

Public finance

Nebraska's Constitution prohibits the state from incurring debt in excess of $100,000. However, there is a provision in the Constitution that permits the issuance of revenue bonds for highway and water conservation and management structure construction. There are $10 million of bonds payable by a separate legal entity that has been blended into the financial activity of the state. These bonds do not represent a general obligation of the state and are secured by revenues from the equipment that the debt was incurred to purchase.

The Constitution also authorizes the Board of Regents of the University of Nebraska, the Board of Trustees of the Nebraska State Colleges, and the State Board of Education to issue revenue bonds to construct, purchase, or remodel educational buildings and facilities. The payment of these bonds is generally made from revenue collected from use of the buildings and facilities. The Legislature has authorized the creation of two financing authorities that are not subject to state Constitutional restrictions on the incurrence of debt. These financing authorities were organized to assist in providing funds for the construction of capital improvement projects at the colleges and the University. Although the state has no legal responsibility for the debt of these financing authorities, they are considered part of the reporting entity.

The Nebraska state budget is prepared by the Budget Division of the Department of Administrative Services and is submitted annually by the governor to the legislature. The fiscal year runs from 1 July to 30 June.

The bulk of general fund monies in 2000/01 were put towards: local tax relief (38%), government (20%), aid to individuals (20%), and post-secondary education (17%). For 2000/01, the general fund was forecast with revenues of almost $2.4 billion, which actually totaled $2.457 billion. In 2001/02, however, general fund revenues fell to $2.363 billion while expenditures shot up to $2.599 billion. In 2002/03, Nebraska's state budget deficit was estimated at 5.9% of the state budget and for 2003/04, it was projected to reach between 21.25 and 28.2% of the state budget.

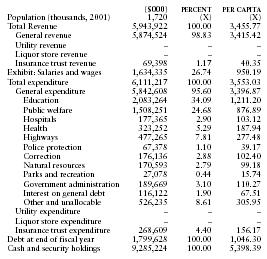

The following table from the US Census Bureau contains information on revenues, expenditures, indebtedness, and cash/securities for 2001.

| ($000) | PERCENT | PER CAPITA | |

| Population (thousands, 2001) | 1,720 | (X) | (X) |

| Total Revenue | 5,943,922 | 100.00 | 3,455.77 |

| General revenue | 5,874,524 | 98.83 | 3,415.42 |

| Utility revenue | – | – | – |

| Liquor store revenue | – | – | – |

| Insurance trust revenue | 69,398 | 1.17 | 40.35 |

| Exhibit: Salaries and wages | 1,634,335 | 26.74 | 950.19 |

| Total expenditure | 6,111,217 | 100.00 | 3,553.03 |

| General expenditure | 5,842,608 | 95.60 | 3,396.87 |

| Education | 2,083,264 | 34.09 | 1,211.20 |

| Public welfare | 1,508,251 | 24.68 | 876.89 |

| Hospitals | 177,365 | 2.90 | 103.12 |

| Health | 323,252 | 5.29 | 187.94 |

| Highways | 477,265 | 7.81 | 277.48 |

| Police protection | 67,378 | 1.10 | 39.17 |

| Correction | 176,136 | 2.88 | 102.40 |

| Natural resources | 170,593 | 2.79 | 99.18 |

| Parks and recreation | 27,078 | 0.44 | 15.74 |

| Government administration | 189,669 | 3.10 | 110.27 |

| Interest on general debt | 116,122 | 1.90 | 67.51 |

| Other and unallocable | 526,235 | 8.61 | 305.95 |

| Utility expenditure | – | – | – |

| Liquor store expenditure | – | – | – |

| Insurance trust expenditure | 268,609 | 4.40 | 156.17 |

| Debt at end of fiscal year | 1,799,628 | 100.00 | 1,046.30 |

| Cash and security holdings | 9,285,224 | 100.00 | 5,398.39 |