Nebraska

Taxation

A constitutional amendment in 1967 prohibited the use of property tax revenues for state government. This forced the passage of both a sales and use tax and an income tax, which had long been resisted by fiscal conservatives in the state. The sales and use tax became effective in 1967, the income tax in 1968.

The state income tax is four-bracket schedule ranging between 2.56% (for a single individual, up to $2,400 of taxable income) and 6.84% (on taxable income above $26,500). Federal adjusted gross income as defined 19 April 2002 can be used as an individual's tax base. The corporate tax rate is 5.58% on the first $50,000 of net income and 7.81% on net income over $50,000. The state sales tax rate was raised temporarily from 5% to 5.5% in 2002, scheduled to fall back to 5% 1 October 2003. Nebraska exempts both foodstuffs and prescription drugs from its general sales tax. Local sales taxes range from none to 1.5%. The state imposes a full array of excise taxes covering motor fuels, tobacco products, insurance premiums, alcoholic beverages, amusements, public utilities, pari-mutuels, and other selected items. In 2002, the cigarette tax was temporarily increased from 34 cents a pack to 64 cents a pack, scheduled to return to 34¢ 1 October 2004. Nebraska's gasoline tax is indexed for inflation, and revised quarterly. The state estate tax (maximum rate 18%) is independent of the federal estate tax, and therefore is unaffected by the latter's scheduled phase-out by 2007. There is also an inheritance tax, collected at the county level. State death and gift taxes constituted 0.5% of state taxes collected in 2002. Other state taxes include an oil and gas severance tax, an oil and gas conservation tax, a uranium severance tax (state severance tax receipts in 2002 totaled $1,221), various license and franchise fees, stamp taxes, and state property taxes. Most property taxes are collected locally. Local tax collections accounted for 43.4% of total state and local totals, in 2000.

The state collected $2.992 billion in taxes in 2002, of which 38.5% came from individual income taxes, 35.7% from the general sales tax, 14.6% from selective sales taxes, 6.5% from license fees, and 3.6% from corporate income taxes. In 2003, Nebraska ranked 16th among the states in terms of its combined state and local tax burden, which amounted to about 9.8% of income.

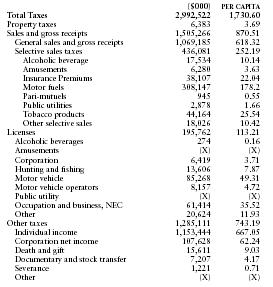

The following table from the US Census Bureau provides a summary of taxes collected by the state in 2002.

| ($000) | PER CAPITA | |

| Total Taxes | 2,992,522 | 1,730.60 |

| Property taxes | 6,383 | 3.69 |

| Sales and gross receipts | 1,505,266 | 870.51 |

| General sales and gross receipts | 1,069,185 | 618.32 |

| Selective sales taxes | 436,081 | 252.19 |

| Alcoholic beverage | 17,534 | 10.14 |

| Amusements | 6,280 | 3.63 |

| Insurance Premiums | 38,107 | 22.04 |

| Motor fuels | 308,147 | 178.2 |

| Pari-mutuels | 945 | 0.55 |

| Public utilities | 2,878 | 1.66 |

| Tobacco products | 44,164 | 25.54 |

| Other selective sales | 18,026 | 10.42 |

| Licenses | 195,762 | 113.21 |

| Alcoholic beverages | 274 | 0.16 |

| Amusements | (X) | (X) |

| Corporation | 6,419 | 3.71 |

| Hunting and fishing | 13,606 | 7.87 |

| Motor vehicle | 85,268 | 49.31 |

| Motor vehicle operators | 8,157 | 4.72 |

| Public utility | (X) | (X) |

| Occupation and business, NEC | 61,414 | 35.52 |

| Other | 20,624 | 11.93 |

| Other taxes | 1,285,111 | 743.19 |

| Individual income | 1,153,444 | 667.05 |

| Corporation net income | 107,628 | 62.24 |

| Death and gift | 15,611 | 9.03 |

| Documentary and stock transfer | 7,207 | 4.17 |

| Severance | 1,221 | 0.71 |

| Other | (X) | (X) |