North Carolina

Taxation

In 1921, North Carolina was one of the first states to adopt a graduated income tax. In 1923, it was one of the first to institute a statewide sales tax. The state and local tax system remains relative centralized, with about 60% of total non-federal taxes collected at the state level. All property taxes, however, are collected locally. In 2001, North Carolina temporarily added an 8.25% bracket for income above $120,000 to its three-bracket personal income tax schedule with rates 6% (up to $12,750 taxable income), 7% and 7.75% ($60,000 to $120,000). The rates are scheduled to decline after 2003. The corporate income tax is a flat rate of 6.9% of net income. Financial institutions are taxed on the basis of their assets ($30 for each $1 million in assets). In 2001, North Carolina increased its state sales and use tax from 4% to 4.5%. Local governments also impose sales taxes, ranging from 2 to 3%. Food, prescription drugs, and certain other articles are exempt from the state sales tax or have lowered rates, but food may be subject to local sales taxes. The state also imposes a wide array of excise taxes covering motor fuels, tobacco products, insurance premiums, public utilities, alcoholic beverages (the state controls all sales), amusements, and other selected items. The cigarette tax, at 5 cents a pack, is the 3rd-lowest in the country (after Virginia and Kentucky). The gasoline tax is indexed to inflation, and contrary to trend elsewhere, was reduced from 24.3 cents a gallon to 22.1 cents a gallon in 2002. The state estate tax, with a maximum rate of 17%, has been de-linked from the exemption for state death taxes in the federal estate tax, which is scheduled to be phased out by 2007. Death and gift taxes accounted for 0.76% of state taxes collected in 2002. Other state taxes include an oil and gas production tax, a forest product assessment tax, various license fees, and stamp taxes.

The state collected $15.535 billion in taxes in 2002 (down from $15.6 billion in 2001), of which 46.7% came from individual income taxes, 21.5% from selective sales taxes 20.6% came from the general sales tax, 5.7% from license fees, and 4.3% from corporate income taxes. In 2003, North Carolina ranked mid-way (25th ) among the states in terms of combined state and local tax burden, which amounted to about 9.5% of income.

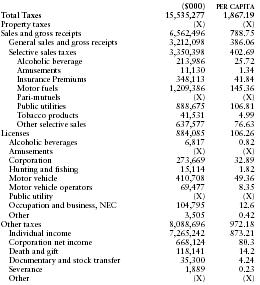

The following table from the US Census Bureau provides a summary of taxes collected by the state in 2002.

| ($000) | PER CAPITA | |

| Total Taxes | 15,535,277 | 1,867.19 |

| Property taxes | (X) | (X) |

| Sales and gross receipts | 6,562,496 | 788.75 |

| General sales and gross receipts | 3,212,098 | 386.06 |

| Selective sales taxes | 3,350,398 | 402.69 |

| Alcoholic beverage | 213,986 | 25.72 |

| Amusements | 11,130 | 1.34 |

| Insurance Premiums | 348,113 | 41.84 |

| Motor fuels | 1,209,386 | 145.36 |

| Pari-mutuels | (X) | (X) |

| Public utilities | 888,675 | 106.81 |

| Tobacco products | 41,531 | 4.99 |

| Other selective sales | 637,577 | 76.63 |

| Licenses | 884,085 | 106.26 |

| Alcoholic beverages | 6,817 | 0.82 |

| Amusements | (X) | (X) |

| Corporation | 273,669 | 32.89 |

| Hunting and fishing | 15,114 | 1.82 |

| Motor vehicle | 410,708 | 49.36 |

| Motor vehicle operators | 69,477 | 8.35 |

| Public utility | (X) | (X) |

| Occupation and business, NEC | 104,795 | 12.6 |

| Other | 3,505 | 0.42 |

| Other taxes | 8,088,696 | 972.18 |

| Individual income | 7,265,242 | 873.21 |

| Corporation net income | 668,124 | 80.3 |

| Death and gift | 118,141 | 14.2 |

| Documentary and stock transfer | 35,300 | 4.24 |

| Severance | 1,889 | 0.23 |

| Other | (X) | (X) |